Today we are breaking down three of the most important metrics shaping the public SaaS landscape today:

- CAC Payback

- Free Cash Flow (FCF) Margins

- Sales & Marketing Spend as a % of Revenue

These metrics are deeply connected - and together, they help explain why SaaS companies are still struggling to grow efficiently in 2025, and why many are shifting from growth engines to cash-flow machines.

We’ll also close with a deeper look into the early signs of circular economics forming in the AI ecosystem - and why the recent GPU leasing news may be a canary in the coal mine.

1. CAC Payback: Go-To-Market Efficiency Is Falling Fast

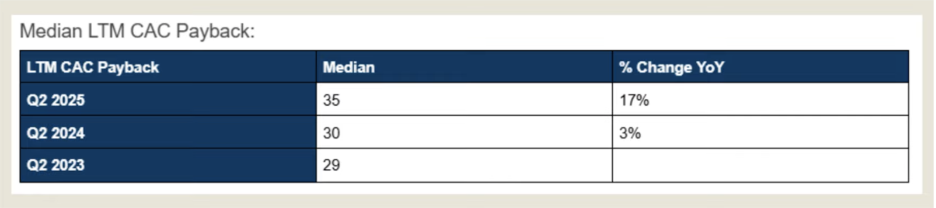

CAC payback has deteriorated significantly over the past two years.

- Q2 2023 median CAC payback: 29 months

- Q2 2025 median CAC payback: 35 months

That’s a 21% increase in the cost to acquire customers in just 24 months.

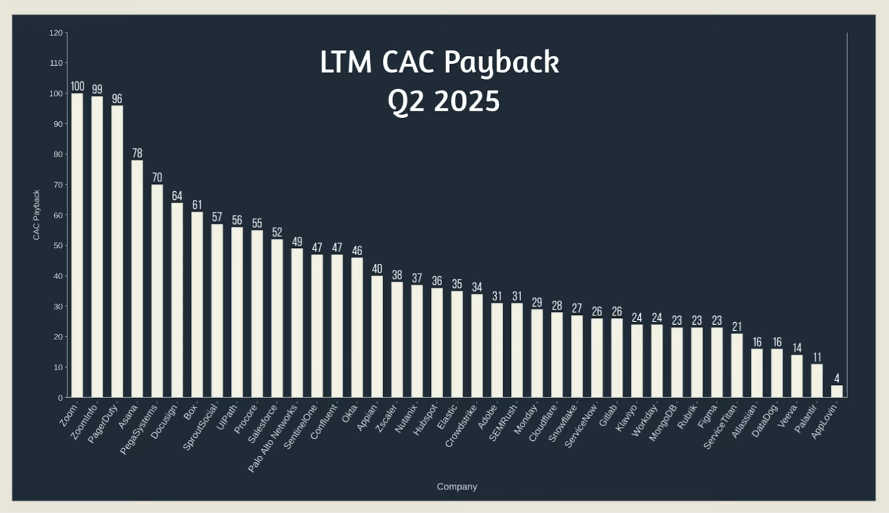

Top performers prove it is possible

Some companies continue to beat the trend:

- AppLovin: 4-month CAC payback (yes, really)

- Palantir: 11 months

- Veeva: 14 months

But the bottom end is shocking

Several companies are now deep into multi-year CAC paybacks:

- Zoom: 100 months

- ZoomInfo: 99

- PagerDuty: 96

- Asana: 78

Even historically strong performers are slipping:

- Sprout Social: 30 → 57 months

- Procore: 30 → 55

- SentinelOne: 30 → 47

- CrowdStrike: 20 → 34

Why this matters:

As CAC payback balloons, growth inevitably slows. And when growth slows, public SaaS companies must re-engineer their margins to keep investors happy.

2. The Growth–Cash Flow Tradeoff

Here’s the dynamic at play:

Falling GTM efficiency → slower ARR growth → pressure for higher FCF margins

In today’s market:

- If you're not growing ARR 30%+,

- Investors expect strong free cash flow margins instead.

And SaaS companies can do this, because most run gross margins above 75%.

The lever they pull? Cutting Sales, Marketing, and R&D.

3. Sales & Marketing Spend Has Fallen 17% in Two Years

Looking at S&M as a percentage of revenue:

- SaaS companies today spend 17% less on S&M vs two years ago.

- And 14% less than just 12 months ago.

Why?

Not because they want to - but because they have to.

When growth stalls, the market demands cash flow. So companies redirect budget from GTM and R&D into margin protection.

The numbers:

- 25 of 40 companies now spend between 33–46% of revenue on S&M

- Only 5 companies spend more than 50%

- In Q2 2023, that number was 12 companies

Only three companies increased S&M spend since 2023:

- Box

- Klaviyo

- Semrush

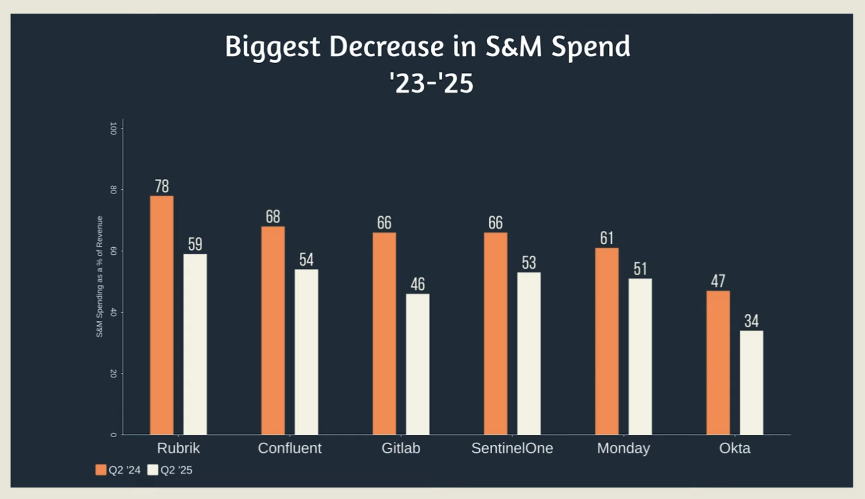

Meanwhile, several companies made massive cuts:

- Rubrik: 78% → 59%

- Confluent: 68% → 54%

- GitLab: 66% → 46%

- Okta: 47% → 34%

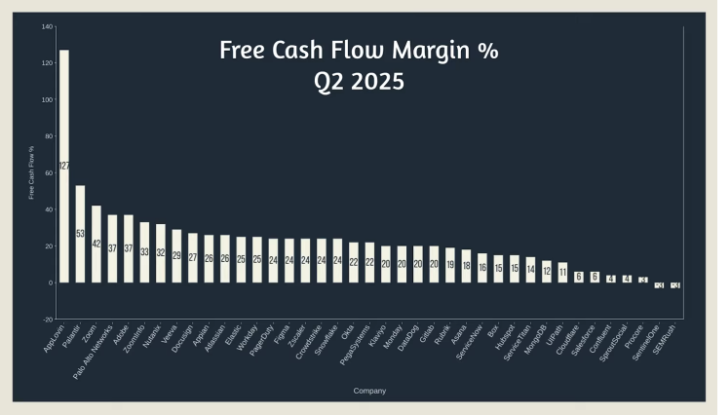

4. Free Cash Flow Margins Are Surging

As expected, reduced GTM/R&D spend is flowing straight into free cash flow.

- Q2 2023 median FCF margin: 14%

- Q2 2025 median FCF margin: 22%

→ A 57% increase in just two years.

Only two companies reported negative FCF in Q2 2025:

- SentinelOne

- Semrush

Compare that to eight companies in 2023.

Notable FCF turnarounds:

- Box: –1% → 15%

- Confluent: –19% → 4%

- Appian: –12% → 26%

- Procore: –10% → 3%

- Figma: –7% → 24%

- MongoDB: –6% → 12%

Again:

These companies would prefer to spend aggressively on growth - but with ARR growth slowing, they’re forced to flip the switch and show cash generation.

5. The AI Bubble’s “Circular Economics” Moment

After the SaaS deep dive, we turned to something new emerging in the AI ecosystem - and it’s starting to look eerily familiar.

Every tech boom eventually shifts from product innovation to financial engineering.

- In the dot-com boom: leasebacks

- In 2008: mortgage-backed securities

- In AI today? Possibly: GPU leasing + closed-loop demand cycles

OpenAI × Nvidia: the GPU leasing idea

OpenAI is reportedly exploring leasing Nvidia GPUs instead of buying them.

On the surface, this reduces capex and gives compute flexibility.

But zoom out, and the picture gets stranger.

The CoreWeave loop

The story looks like this:

- Nvidia invested in CoreWeave

- CoreWeave used Nvidia GPUs as collateral to borrow money

- CoreWeave used that money to buy more Nvidia GPUs

- Nvidia then had to backstop CoreWeave’s IPO

- The stock inexplicably tripled afterward

That’s not organic demand - that’s circular economics.

Add in the leasing model…

Now Nvidia appears to be reinventing itself as a financier, leasing its own chips to AI customers to maintain demand.

At the same time:

- Oracle is reportedly struggling to find buyers for the GPUs it already purchased

- Nvidia’s yearly upgrade cycle means GPU value decays fast

- Nvidia is the bellwether of the US market - cracks here shake everything

These are the kinds of signals you see when an innovation cycle begins to turn into a financial one.

Conclusion: A Warning Sign or Smart Capital Allocation?

The SaaS metrics paint a clear picture:

- CAC paybacks are blowing out

- Growth rates are slowing

- S&M spend is falling

- Free cash flow margins are rising

SaaS is in a defensive posture - using its high gross margins to satisfy markets while GTM efficiency struggles.

Meanwhile, the AI ecosystem shows early signs of circular financing that could indicate we’re late in the cycle.

Is it a warning sign?

Or just a creative, capital-efficient way to access compute?

Time will tell.

If you haven’t already, download the full Q2 State of SaaS Report to dive deeper into the data and company-by-company breakdowns.

Thanks for reading.

Meet with our founder

Want to meet to discuss what an outbound engine would look like in your business?