Public SaaS earnings season always reveals where the market is heading - and Q2 2025 gave us one of the clearest pictures yet of how growth, efficiency, and investor expectations are shifting.

In this breakdown, we’re looking at four companies that tell the story of the current SaaS landscape better than just about anyone: Rubrik, Asana, PagerDuty, and UiPath.

We’ll also look at early data from our upcoming Q2 State of SaaS Report, specifically how ARR growth rates are trending across the 40 public SaaS companies we track.

Let’s dive in.

PagerDuty: When Growth Slows, the Whole Machine Struggles

PagerDuty is a perfect example of what happens when a SaaS company loses its growth momentum but keeps spending like the old days.

Over the past 12 months, they added just $30M in net new ARR - while spending $203M on Sales & Marketing. That disconnect shows up everywhere in the metrics.

Q2 highlights:

- ARR growth: 6% YoY

- Net new ARR: $30M

- CAC payback: 96 months

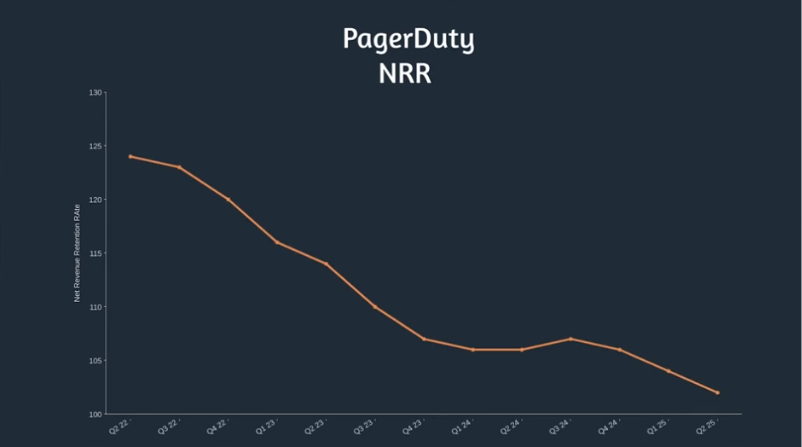

- NRR falling from 126% → 102%

- RPO growth: 5% YoY

But it’s not all doom and gloom. PagerDuty has aggressively refocused on efficiency:

- Free cash flow margin improved from 1% → 24%

- Operating margin turned positive for the first time (+3%)

- Cash generation is stabilising the business

Still, with the company valued at ~3× ARR, the market is clearly expressing caution. Until growth returns, PagerDuty stays in “rebuild mode.”

Rubrik: A Rare Example of Hypergrowth at Scale

Rubrik continues to be one of the most impressive growth stories in SaaS - and Q2 solidified its position as a category leader.

Q2 highlights:

- ARR: $1.19B

- ARR growth: 55% YoY

- Net new ARR: $423M (second-highest in all public SaaS)

- CAC payback: 23 months

- Magic number: 0.64

Rubrik’s path has always involved heavy spending. But they’re finally bending their cost curve:

- S&M: 82% → 59% of revenue

- FCF margin: 19%, marking the 4th straight quarter of positive FCF

- Operating margin improving but still –30%

At a valuation of 14× ARR, the market is expecting Rubrik to keep delivering elite growth. Any slowdown will force rapid tightening - but for now, they’re executing.

Asana: Low Growth, Big Cuts, Promising Signals

Asana has been grinding through a long stretch of single-digit growth - but Q2 finally showed early signs that a turnaround might be on the way.

Q2 highlights:

- ARR growth: 10% YoY (slight improvement)

- Operating margin: improved from –43% → –25%

- Market cap: $3.28B (~4× ARR)

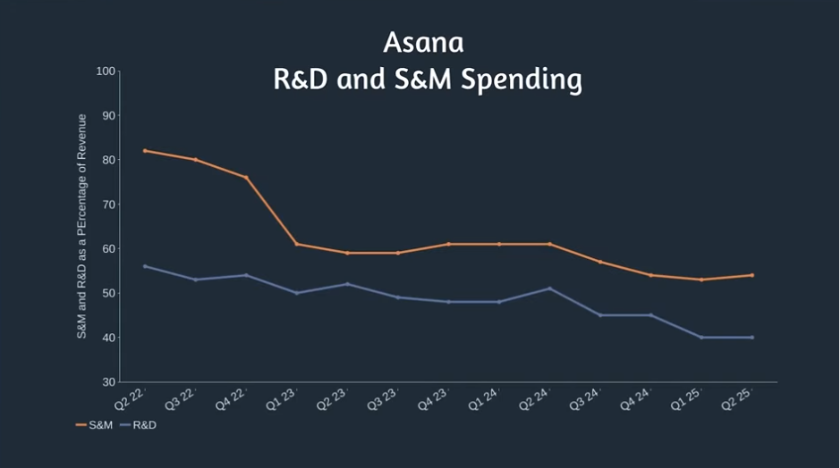

Much of the margin improvement is powered by aggressive cost reductions:

- S&M down to <60% of revenue

- R&D down to 42%

The leadership reboot matters here:

- New CEO Daniel Rogers is pushing hard into enterprise

- New CFO Sonalee Parekh has a track record of scaling profitably at RingCentral

And we’re starting to see the impact:

- Highest logo retention in Asana’s history

- NRR ticking up from 95% → 96%

- $100K+ customers growing 19% YoY

It’s still early, but the direction is finally changing.

UiPath: Efficiency Up, Growth Down

UiPath has been on a multi-year mission to tighten spend, rebuild its go-to-market engine, and become more enterprise-focused. And while efficiency is improving, growth remains the challenge.

Q2 highlights:

- ARR growth: 11% YoY (down from 19%)

- Net new ARR: $172M over the past 12 months

- S&M spend: $718M

- CAC payback: 56 months

- Operating margin: –5% (up from –33%)

They’ve cut heavily into spend:

- S&M as % of revenue: 61% → 46%

- R&D: 31% → 27%

Pipeline is strong, but deal cycles remain long - especially at the high end of the market. With the company trading at 3.8× ARR, expectations are muted.

The Bigger Picture: SaaS ARR Growth Is Slowing Everywhere

Across the 40 public SaaS companies we track, the trend is extremely clear: ARR growth has been steadily declining for two years.

Median ARR growth:

- Q2 2025: 20%

- Q2 2024: 23%

- Q2 2023: 25%

Even the strongest companies aren’t immune:

- Atlassian: 34% → 23%

- CrowdStrike: 32% → 20%

- SentinelOne: 32% → 22%

- Zscaler: 30% → 21%

But there are outliers:

- AppLovin: 44% → 77%

- Palantir: 27% → 48%

- Box: 3% → 9%

- ZoomInfo: 3% → 5%

The message is clear:

Growth is harder to find - and increasingly concentrated.

Meet with our founder

Want to meet to discuss what an outbound engine would look like in your business?