Q2 earnings are in, and one thing is painfully clear:

the market no longer rewards “pretty good.”

Across Elastic, Nutanix, Zscaler, GitLab, ServiceTitan, and Figma, you can see the same pattern over and over again:

- Strong efficiency is no longer enough.

- Clean execution is no longer enough.

- Even 20% ARR growth - once elite - is barely table stakes.

We are officially in a barbell market. At one end: companies growing 30–50% with best-in-class efficiency. At the other: those struggling with slowing expansion, heavier go-to-market motion, or messy cost structures.

Everyone else? The market is compressing their multiples into the floor.

Here’s how that played out in Q2.

Elastic: Great Business, Average Growth, Compressed Multiple

Elastic is what investors used to salivate over:

- 20% ARR growth at billion-dollar scale

- CAC payback of 22 months

- 25% FCF margin

- Rule of 40 in the mid-40s

- ARR per employee over $400K

Five years ago, this gets you a 12×+ ARR multiple.

Today? Around 6×.

Elastic isn’t doing anything wrong - in fact, they’re running a tight, well-operated business. But the gravitational pull of today’s market is different. With AI-native companies growing 200–300% and grabbing headlines, 20% simply won’t earn a premium.

Elastic is a reminder that in this cycle, quality doesn’t equal multiple expansion.

Velocity does.

Nutanix: The Quarterly CAC Payback That Broke Finance Twitter

Nutanix had one of the wildest single-quarter CAC paybacks we’ve seen: 142 months.

That number alone is enough to make any GTM leader spit out their coffee - but it’s also misleading. A single quarter doesn’t tell the story. The trailing 12-month CAC payback comes in at a much healthier 37 months, and almost every operational metric is trending up:

- S&M as % of revenue down from 54% in 2022 to 43% now

- Operating margin flipped positive

- FCF margin: 32%

- Rule of 40: 51

Nutanix is a slow grower in a flashy market, but they’re executing a genuine turnaround. Still, with ARR growth sitting below 20%, investors won’t reward them beyond an 8× ARR multiple.

Again: the growth bar is higher now.

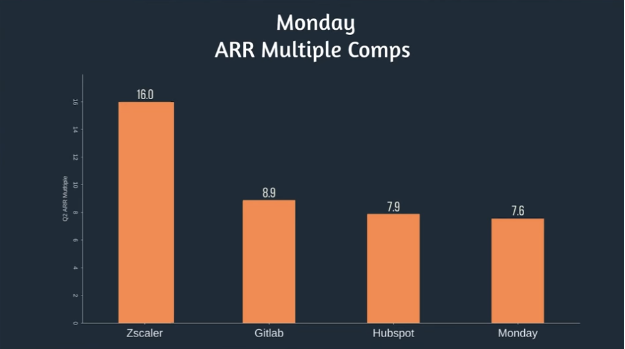

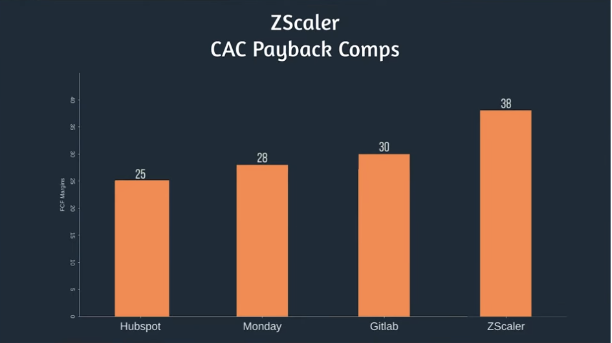

Zscaler: A Premium Multiple Without the Premium Growth

Zscaler sits near the top of the SaaS valuation stack:

- Market cap: $47B

- ARR multiple: 16×

That’s nearly double what similar-scale companies like HubSpot, Monday.com, and GitLab trade at.

But Q2 didn’t provide much justification for that premium.

Growth was fine - but not exceptional:

- ARR growth: 21%

- Net new ARR: $505M

- CAC payback: 38 months (worse than peers)

Efficiency wasn't enough to offset the growth concerns:

- FCF margin: good, but not market-leading

- Operating margin: –4% (up slightly from –5%)

- ARR per employee: $362K (well below the public SaaS median of $416K)

The story is unchanged: great brand, strong security footprint, but the numbers simply don’t match the valuation. And in a market this unforgiving, “good” won’t justify “premium.”

Unless growth accelerates meaningfully, Zscaler’s multiple will remain under pressure.

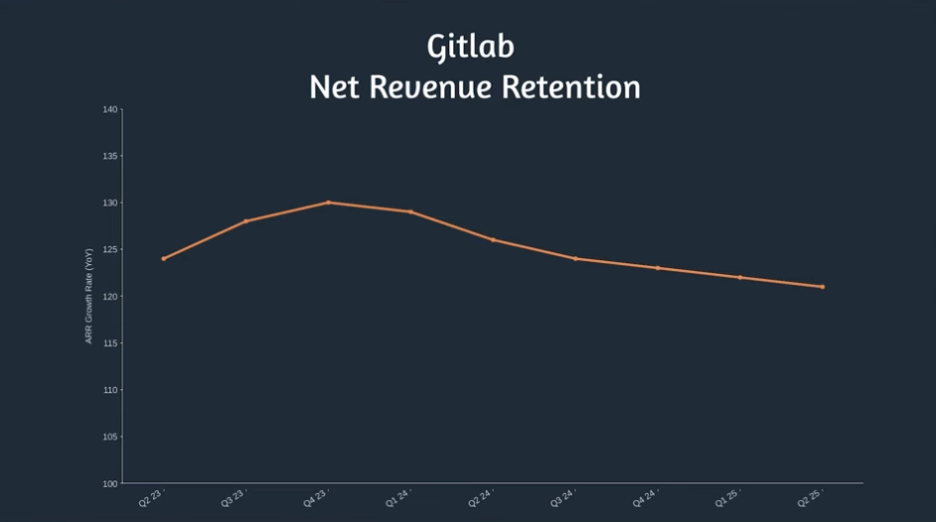

GitLab: The Cleanest Operator in Public SaaS Right Now

GitLab continues to be one of the cleanest operators in public SaaS.

Retention remains elite

- NRR: 122%

- Down slightly from 126% last year, but still world-class

Growth remains well above the public SaaS median

- ARR growth: 29% (vs the 19% median)

- Net new ARR: $214M YoY

Go-to-market efficiency improving

- S&M: 46% of revenue (down from 54%)

- R&D: 30% (down from 34%)

- G&A: 19% (down from 24%)

- CAC payback: 26 months

- Magic number: 0.80

Other highlights

- Operating margin: –8% (up from –22%)

- Rule of 40: 49

- Rule of X: 78

- RPO growth: 32% YoY

- ARR multiple: ~9×

A high-quality quarter from one of the most consistently strong performers in public SaaS.

GitLab doesn’t have the hype of the AI darlings, but it is quietly developing one of the strongest combinations of growth + efficiency in public markets.

It’s the opposite of Zscaler: a reasonable multiple for an arguably underrated operator.

ServiceTitan: The Growth Is There - The Cost Structure Isn’t

ServiceTitan recently joined the public markets after a long private journey - 17 years from founding to IPO. Now at $930M ARR, they’re growing a healthy 26%.

Go-to-market is efficient

- Net new ARR: $191M

- S&M spend: $265M

- CAC payback: 21 months

- Magic number: 0.72

- NRR: 110%

But Opex is heavy

- Operating margin: –14%

- FCF margin: 14%

- Rule of 40: 40

- Rule of X: 66

The standout red flag:

- G&A at 26% of revenue

Comparable companies at similar scale sit between 13–19%. That level of overhead will need to come down for margins to improve.

Valuation

- Market cap: $10.7B

- ARR multiple: 11.5×

Strong business, but some operational tuning is required.

Figma: A Brilliant Quarter Overshadowed by One Number

Figma’s first quarterly earnings as a public company were volatile.

After the Q2 report, shares dropped 20% - primarily because of a lower-than-expected Q3 forecast:

- Q3 ARR growth guidance: 33%, down sharply from

- Q2 ARR growth: 41%

But the actual Q2 results were excellent

- Net new ARR: $290M YoY

- Net new ARR: $86M QoQ

- CAC payback: 11 months

- Magic number: 1.25

- FCF margin: 25%

- Operating margin: 1%

- ARR per employee: $606K (elite)

When zooming out:

- 12-month CAC payback: 23 months (more normal)

The key question now:

Can Figma keep ARR growth above 30% - and for how long?

Every SaaS company eventually faces ARR deceleration. Figma is no exception. How they manage that curve will determine the stock's long-term trajectory.

The Big Picture: SaaS Is Becoming Binary

Across all six companies, the story is the same:

1. Growth above 30% = rewarded

GitLab, Figma (until guidance), AI-native companies

2. Growth around 20% = punished

Elastic, Nutanix, Zscaler

3. Efficiency matters - but only after growth

Strong FCF margins or good CAC payback won’t earn you a higher multiple unless you have velocity to match.

We’re in a market where:

- Customers are cautious

- Sales cycles are long

- AI companies are distorting growth benchmarks

- Investors want clean, profitable execution

- And anything not in the top quartile gets compressed

The takeaway?

The middle of the market has disappeared.

If you’re not growing fast, you better be extremely efficient - and even then, you’re fighting gravity.

Meet with our founder

Want to meet to discuss what an outbound engine would look like in your business?